Are data centres core infrastrucutre?

With the AI boom underway, demand for data centre capacity is continuing to accelerate. We often get asked the question: are data centres core infrastructure? For large physical assets, a common assumption is that data centres are core infrastructure in the same way that a utility or a toll road is fundamentally a core infrastructure investment. However, as specialist managers, we view the risks and opportunities of data centres as fundamentally different from core infrastructure assets.

In this report, we explore this topic. In short, from our perspective, it is much more than the physical characteristics of an asset that determine the investment appeal of an asset. Core infrastructure assets are instead characterised by their ability to generate high-quality earnings – those generated by dependable demand and underpinned by predictable cash flows. The question is therefore: ‘do data centres deliver this type of profile to investors and what underpins them?’

Demand for data centres is unprecedented

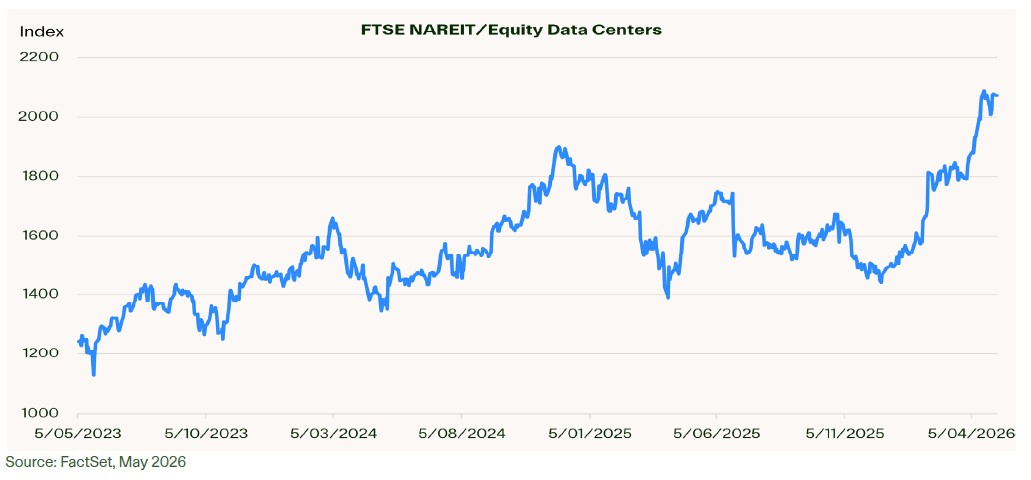

First, to set the scene. AI is driving unprecedented demand for data centre capacity. Global AI data centre capacity grew from around 0.15 GW in early 2022 to 29.6 GW by the end of 20251, representing a near 200-fold increase over this period. The swift upturn in demand is reflected in the share price performance of listed data centre assets; the FTSE NAREIT Data Centers Index is up around 65% in three years. AI is a major driver, with all the global digital activity such as cloud computing applications also contributing to fast-paced demand.

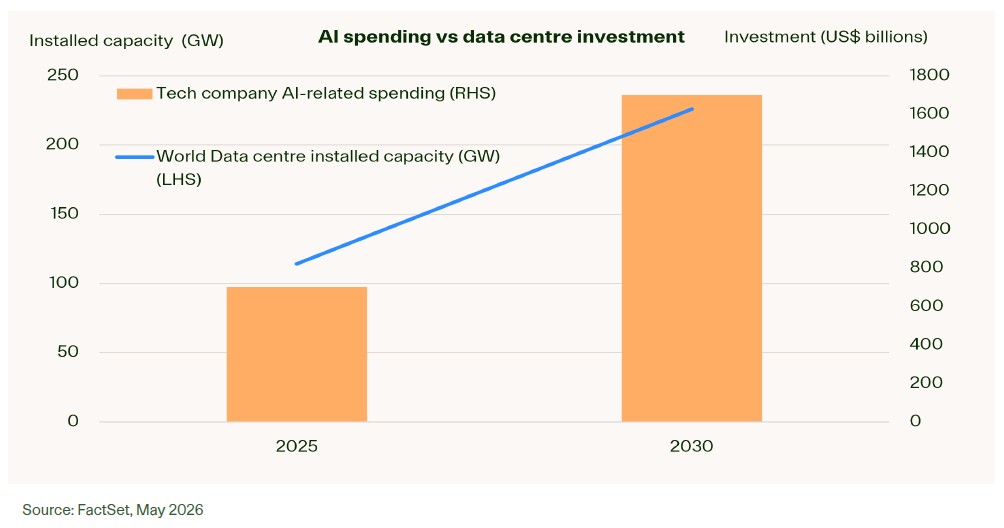

Looking to the future, estimates for data centre growth and tech/AI investment move hand in hand. AI-related spending for technology companies globally was estimated to be US$700 billion in 2025, with global AI capex spending estimated to be more than US$500 billion. By 2030, spending is projected to increase to US$1.7 trillion or more for AI-related technology spend, and US$1.3 trillion2 for AI capex. In lockstep, total world data centre capacity (including AI data centres) is expected to grow from 114 GW in 2025 to 225 GW3 in 2030. The scale of activity and forecast increases is staggering. Demand growth reflects accelerating user volumes and also growth in more intensive applications such as generative AI.

Digital…and infrastructure

We see data centres as sitting within a wider digital investment umbrella, which can include the data centres themselves, 5G networks, fibre, satellites and broadband networks along with virtual infrastructure, which includes cloud computing platforms and cybersecurity frameworks.

In our view, data centres are most certainly part of this broader digital investment landscape but are not core infrastructure. Recall that an infrastructure asset, to meet our definition, has to meet specific criteria that lead to reliable earnings through the economic cycle and don’t relate just to the physical characteristics of the asset. We look for several key attributes in an asset to consider it core infrastructure:

- demand: The first thing that we look at is whether the asset is essential for the efficient function of a community. If people must use the asset as part of their everyday life, then we know that the demand is predictable.

- cash flows: The next thing that we look for is assets with earnings that are not sensitive to three key factors: competition, commodity price movements or sovereign risk. An asset that can satisfy these requirements has the potential to generate stable cash flows to an investor through the investment cycle. This is the ultimate purpose of infrastructure in an investment portfolio.

Using this approach, there are three reasons data centres are not core infrastructure. First, data centre assets do not have a sustainable competitive advantage. At this moment, there is an enormous wave of demand for these assets. However, absent this demand the competitive advantages are limited. Within the listed data centre universe, there is significant variation today in competitiveness across the data centre assets within a given company. In the top tier are those assets that have a connectivity advantage, which means they have the lowest-latency service. These companies have land in opportune areas (for example, close to major metro areas, close to key end-users), have access to power and can offer a connectivity-rich environment for tenants within their data centres, such as those that have high-quality enterprise and cloud companies co-located. The ability to provide a connectivity ecosystem for tenants is currently a powerful advantage. Lower-tier facilities do not have this moat. This includes centres on the outskirts of smaller metro areas or those with a fragmented tenant base. These data centres are exposed to competition. They are typically commodity-like in that they provide a replicable service to their customers/tenants, suggesting limits on their market power over time.

We note that while demand for data centre capacity outstrips supply, data centres retain an advantage in the marketplace. Once that balance shifts – and we do not know when that might occur – there are risks to the competitive advantages outlined here. For example, we could see a migration from smaller centres near metro areas to large campuses in locations further afield. The evolution in AI workloads could also be instrumental should latency become less of a driver for close proximity.

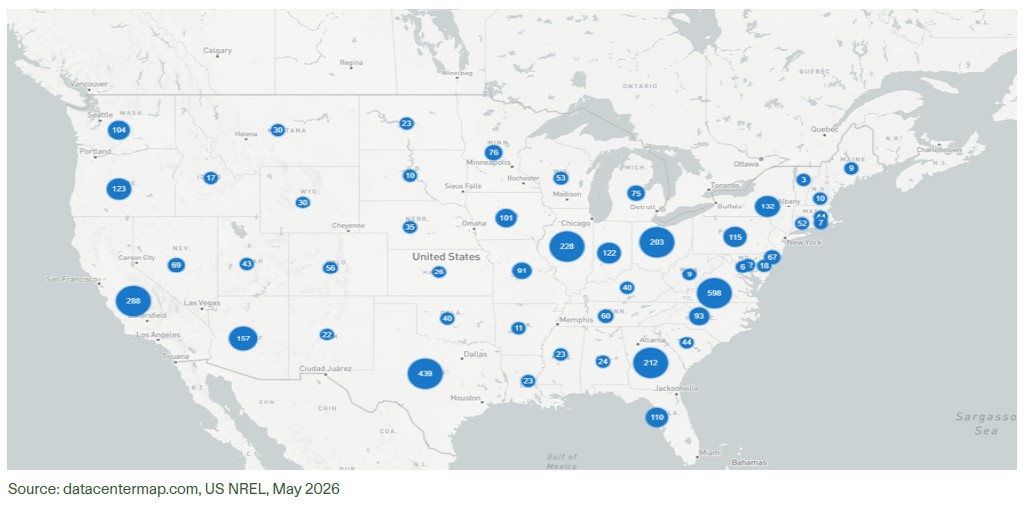

For the United States, the largest data centre market, there are more than 3,000 operational data centres and that number is expected to grow substantially in the years ahead, with more than 1,500 new data centres in various stages of development nationwide4. Development is becoming more dispersed, as space is at a premium in some saturated markets (e.g., Texas, Virginia). The build of speculative capacity in so-called ‘tier 2’ and ‘tier 3’ markets underscores the risk to these assets in future, particularly if the demand-supply balance is flipped. At the same time, while regional clusters are in a relatively attractive position today due to supply/demand dynamics, this is not unconstrained. Older facilities near large metros that may have had a first-mover advantage also face obsolescence risks, particularly if moving out to a larger, newer facility becomes more tenable for centre tenants. These facilities risk losing occupancy and pricing power as more competitive assets become available. For example, many such facilities pass through power costs to tenants, and the older generation of these assets means they can be less energy efficient than newer builds. Erosion in demand and discounting are future competitive headwinds to consider. At present, there is a tidal wave of demand for data centres, which serves to diminish these risks. We do not know if or when this may turn. However, the very fact that it could gives us caution given the high volume of facilities that could potentially compete against others. We also note that an established toll road or an airport, for example, does not face this dynamic.

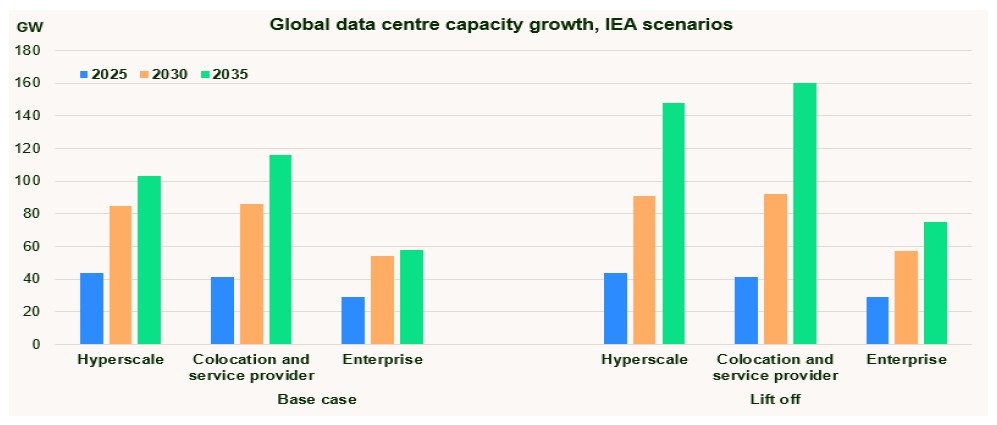

The second related reason is the risk to these assets in terms of the large upfront capital expenditure they require. While it is true that high capital costs are common for infrastructure projects, these assets have a competitive position or operate in a regulated framework such that we have confidence they can recover their upfront investment. Data centres, in contrast, are exposed to competition, are unregulated and are incredibly capex-intensive. As a result, this presents a risk to cash flows to investors. High-spec data centres have high capital costs. The expected growth in installed capacity, from an estimated 114 GW in 2025 to 225 GW by 20305, implies investment of close to US$4 trillion in data centres in the next five years, with more than half of this outlay expected to come from co-location/service provider and enterprise data centres, including those in listed data centre company portfolios. Should we see greater AI adoption than forecast under this International Energy Agency (IEA) base case, this would imply even more investment in the subsequent five-year period. For example, the ‘lift off’ scenario forecast by the IEA suggests 7% more in total installed capacity in 2030 and 38% more in 2035.

Source: IEA, May 2026. Per the IEA, The Base Case provides the central projection and considers trends in AI development, investment, and bottlenecks in energy and IT supply chains. The Lift-Off Case explores the impact of stronger AI adoption and increased global demand for digital services, leading to even stronger deployment of data centre facilities than in the Base Case.

It assumes that bottlenecks can be effectively resolved over time, with increases in manufacturing capacity for chips and energy equipment, and policy progress and innovation easing constraints such as grid connection wait times.

In looking at forecast capital investment for data centres, what is clear is that expectations are strong. Not only are the figures large, but the time frame for such large investment outlays is short. Projects of this size and scope have high upfront costs and long lead times, meaning that capital is going to be outlaid thick and fast, potentially exposing investors to development risk. Data centre developers and owners do have some protection in the form of contracts. However, the coverage provided is variable and is different from a regulated model that guarantees a return on agreed capex. Hyperscalers, as high-quality tenants, typically lease capacity for an initial 8- to 15-year term, and many data centres look to pre-lease the majority of capacity before construction commences. Such assets can be of interest to infrastructure investors in that they provide surety of return on capital. However, finding a listed entity with a portfolio of these well-structured assets is difficult. There is considerable variability in contract models, with medium-sized tenancies typically leased for a shorter initial term of 6-9 years, and many data centres tenanted on initial three-year term contracts with one-year renewals (such as for retail co-location and small enterprise data centres). Shorter-duration contracts mean more churn, creating more risk for a data centre developer. Furthermore, longer-term contracts are typically associated with high-quality tenants, namely hyperscalers, who themselves have immense bargaining power and are also moving to develop their own campuses and on-site generation. These contracts carry the risk that the hyperscaler could drop back its demand, resulting in subleasing or empty capacity.

The specific nature of the use for data centres is an added element of risk to the large capital expenditure profile for these assets. Data centres are built for a particular use and are not easy to repurpose should demand fall short. Even for an asset with a 15-year pre-lease, there is no guarantee the site can be re-leased following the conclusion of this initial term. Asset obsolescence is a real risk at the end of a lease term, which in turn drives the need for upgrades to the technology stack and facility going forward, along with a haircut to yield.

Demand for on-site generation, which also reflects the specific needs of data centre assets, adds to the scale of capex and the associated risk. Where data centre expansion is rapid and outpacing grid development, some developers are looking to add on-site generation. (In the United States, this is mainly natural gas.) While such projects are early stage, they would nonetheless add substantial cost to the overall capital outlay for a data centre site.

The third reason we do not consider data centres to be core infrastructure is dependable demand. By this, we mean demand that is sufficient and also long-standing enough to sustain data centres as an asset class. While data sovereignty, digitalisation, cloud computing and AI support demand for data centres, technological change is rapid; looking out five years from now, it is hard to say that demand for data centres will continue along the path we expect (compared with, for example, demand for a water utility, electricity utility or a major airport). It is not that we cannot see robust demand now, but that there is a wide range of outcomes for demand growth in the future that does not fit with the defensive return profile of core infrastructure. In particular, with AI evolving rapidly, there are risks to cash flows from these assets from a structural shift in demand. Should the tide turn on demand for these facilities, developers or data centre companies could be left holding unused or partially complete assets into which they have sunk significant capital. A good example of this was the release of the DeepSeek R1 model in January 2025, which was far more efficient than many other AI models when it was released.

This shook assumptions that surging AI demand would mean ongoing, robust demand growth for data centres. The market reaction was telling, with the FTSE NAREIT Data Centers Index down 20% from the start of December 2024 to the end of March 2025.

A powerful infrastructure opportunity

Given the risks to cash flows outlined above, we do not see data centres themselves as infrastructure. Instead, we look at the infrastructure opportunity presented by data centres through the lens of power demand. Data centres are a driving force for power demand, which creates a meaningful opportunity for regulated utilities serving these end users.

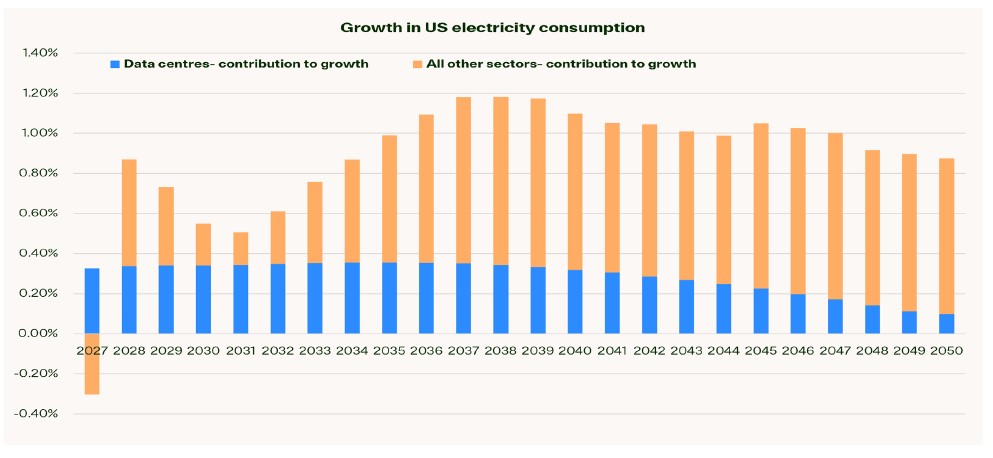

Indeed, data centres are expected to be a major driver of electricity consumption in the coming decades. The US, a major data centre market, is a key example. Data centre electricity consumption accounts for an outsized proportion of expected growth in electricity demand in the US from 2027 to 2050. Their consumption contributes around 0.25 percentage points to annual US electricity demand over this time frame. Considering total demand growth is projected to average ~1.0% over this horizon, data centres will generate a significant portion of total growth.

Source: US Energy Information Administration, Magellan analysis, May 2026

Given the size of the US market, this represents substantial scale-up in power generation capacity in the coming decades. To meet expected demand just from data centres, an additional ~75 GW of electric power is required by 2030 and ~240 GW by 2040 compared with 20256 levels (when US data centres consumed an estimated 105 GW of electricity). This is not just a US phenomenon. For example, the Australian Energy Market Operator (AEMO) projects that energy consumption from data centres in Australia could almost double by 2030. There is a similar pattern of expected rapid growth in power demand in other major economies globally.

For infrastructure, this outlook points to significant capital expenditure to expand generation and grid capacity in the coming 5-10 years. For regulated utilities, more capital expenditure is an opportunity and a positive for those companies affected. In a regulated utility model, investment is undertaken under an approved capital investment plan, meaning the utility can earn an agreed rate of return on its investment, as determined with the utility’s regulator. In this context, the utility grows its earnings to shareholders at a healthy pace, as the regulated asset base on which it earns a return expands. We see multiple examples of this dynamic across US regulated utilities. For example, US integrated power company Evergy reported a $21.6 billion capex plan and 6-8% earnings per share growth for the 5-year period to 2030. WEC Energy, another US integrated power company, has $37.5 billion in capex and 7-8% earnings per share growth guidance for 2026-2030.

The obvious question on the above is what then happens to power demand, to capital investment and ultimately to cash flows to investors if data centre demand cools off? This is where the definitional piece of infrastructure is incredibly important. Regulated assets earn an agreed rate of return on capital invested; even if the pipeline diminishes, capital invested to date earns a return. In the future, these companies can diversify.

Looking to the US again, recall that data centres are ~25% of annual demand growth in the next two decades. This is high, but it is not the only driver; the other 75% still needs to be met. Accordingly, regulated utilities can refocus their capital investment plans on other growth drivers, including other end-users (such as industrial or manufacturing) or other purposes, including asset replacement, upgrading and investment in renewables. We note that even before the AI/data centre phenomenon, these regulated utilities had solid capex programs and were earning healthy returns on capital. There is a demonstrable alternative for these companies to continue to generate earnings growth, even if the data centre pipeline deflates.

We also note that while the data centre pipeline is not certain, the density of the demand at these sites is not expected to diminish in a hurry, which supports the robust outlook for power demand. Data centres are not energy-efficient assets, with cooling systems and servers along with the other equipment drawing heavily on power. Energy efficiency is expected to improve; for example, US power usage effectiveness is expected to increase by ~1.0% per year from 2025-20357. However, this is more than offset by the growing proportion of AI workloads that require 3-5 times more energy than other less complex queries. Growth in this sub-sector means higher potential power needs for cooling systems, IT, and to serve the facility design. AI data centres also have more variable electrical loads, given their use of high-grade GPU chips and the clustering of these chips. This drives the need for higher power density overall. In addition, grid infrastructure remains a key pinch point that will likely require robust investment in the coming years, even if data centre growth were to plateau. With AI models driving swings in power demand, there are implications for grid stability, with more sophisticated grid infrastructure an important backstop. So while the overall pipeline for data centres could slow, this could be decoupled somewhat from the facilities’ power requirements.

Investing in affordability

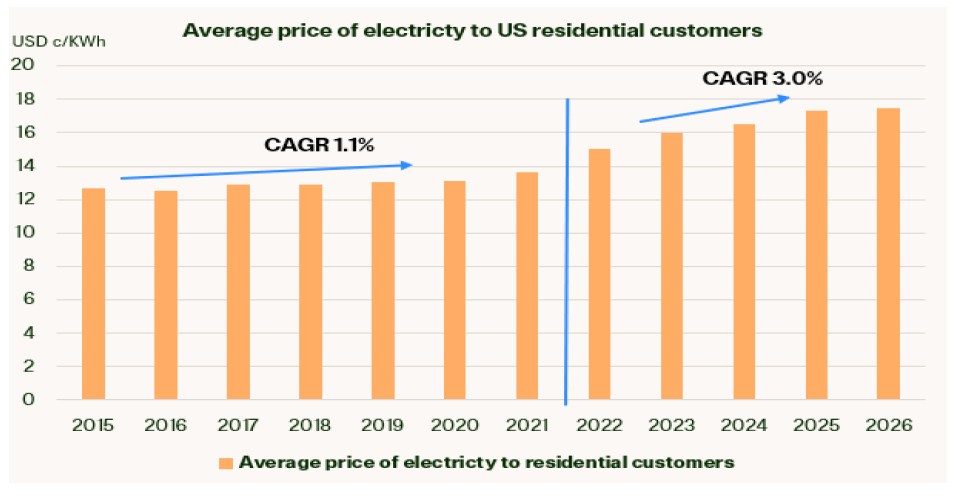

The outlook is compelling for power demand and for regulated utilities on the back of data centre growth. While well-insulated from competition and well-supported by customer demand, for these companies customer affordability is one key risk. Customer power prices have gone up as demand has gone up, notably in the US.

Source: US EIA, May 2026, Magellan analysis

At 3%, annual electricity price growth since 2022 for US households is not outsized compared to overall consumer inflation. Still, data centres are a highly visible flashpoint for concerns about energy prices and household affordability issues. The upturn in power prices is a risk to regulated utilities should the drumbeat on affordability get louder. Regulators pay attention to constituents’ concerns, and this can be expected to be a key consideration in upcoming rate case determinations. We could see downward pressure on allowable rates of return, constraining earnings growth. So far, this impact has been marginal, though this is an issue that bears monitoring.

Over a longer time frame, this headwind could dissipate and potentially become a tailwind. The introduction of large-load tariff structures and debate on US state-level reforms to support such special tariffs are key developments in recent months. There were 29 of these tariffs approved in the US in 2025, as compared to 1-2 a year for the prior decade8. For example, the US state of Virginia has approved a new rate class for large-load customers that will take effect in 2027. Some US regulated utilities have proposals underway for more such mechanisms in their service territories. Xcel Energy has proposed new large-load tariffs in Minnesota, Wisconsin, Colorado and Texas. These plans limit or flatten the impact on retail rates, with the potential for cost savings to retail customers in the future.

Data centres are a structural force for infrastructure investment

The common conception of data centres as core infrastructure is not one we share. From our perspective, we do not view the underlying economics of the sector as anywhere as attractive as the competitive advantages of regulated utilities, established toll roads or other core infrastructure assets. A further challenge is that listed companies have ownership of diverse assets, not just the one asset. If this were a portfolio of tier 1 data centre assets with long-term, high-quality counterparties, that would represent a meaningfully more attractive proposition than a listed company with a more diverse group of assets, with varying quality. What is available in the listed market is also very important to the investment outcomes, given the sector’s economics. Looking closely at the characteristics of their business models, we see opportunity not in direct investment in data centres but in the regulated utilities that power them. With the ability to earn a guaranteed return, to flex investment and, in many cases, to adapt tariffs to suit, these utilities show us a powerful opportunity. We do not know the future for AI, but from where we stand today this is a compelling way to play into this trend, and one that appears durable over time.

By The Magellan Infrastructure Team

1 Stanford University, Stanford AI Index [https://hai.stanford.edu/research/ai-index]

2 International Energy Agency, UBS, McKinsey, Magellan analysis

3 International Energy Agency

4 Pew Research Center. Data centres in development included in this count are those under construction, planned or land-banked.

5 International Energy Agency

6 US Energy Information Administration

7 International Energy Agency

8 Smart Electric Power Alliance, Utility Dive, May 2026

Important Information:

This material is not intended to constitute advertising or advice of any kind and you should not construe the contents of this material as legal, tax, investment or other advice. In making an investment decision, you should read and consider any relevant offer documentation applicable to any investment product or service and must rely on your own examination of the same and consider obtaining professional investment advice tailored to your specific circumstances before making any investment decision.

The investment program of the strategy or strategies presented herein ('Strategy') is speculative and may involve a high degree of risk. The Strategy is not intended as a complete investment program and is suitable only for sophisticated investors who can bear the risk of loss. The Strategy may lack diversification, which can increase the risk of loss to investors. The Strategy's performance may be volatile. Past performance is not necessarily indicative of future results and no person guarantees the future performance of the Strategy, the amount or timing of any return from it, that asset allocations will be met, that it will be able to implement its investment strategy or that its investment objectives will be achieved. Statements contained in this material that are not historical facts are based on current expectations, estimates, projections, opinions and beliefs and such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. This material may contain ‘forward-looking statements’. Actual events or results or the actual performance of the Strategy or any financial product or service may differ materially from those reflected or contemplated in such forward-looking statements. The Strategy will have limited liquidity, no secondary market for interests in the Strategy is expected to develop and there are restrictions on an investor's ability to withdraw and transfer interests in the Strategy. The management fees, incentive fees and allocation and other expenses of the Strategy will reduce trading profits, if any, or increase losses.

No representation or warranty is made with respect to the correctness, accuracy, reasonableness or completeness of any of the information contained in this material. This information is subject to change at any time and no person has any responsibility to update any of the information provided in this material. This material may include data, research and other information from third party sources. No guarantee is made that such information is accurate, complete or timely and no warranty is given regarding results obtained from its use. The issuer of this material and its related entities and affiliates will not be responsible or liable for any losses, whether direct, indirect or consequential, including loss of profits, damages, costs, claims or expenses, relating to or arising from your use or reliance upon any part of the information contained in this material including trading losses, loss of opportunity or incidental or punitive damages.

This material and the information contained within it may not be reproduced, or disclosed, in whole or in part in any circumstances. , Further information regarding any benchmark referred to herein can be found at www.magellaninvestmentpartners.com/funds/benchmark-information/. Any third-party trademarks contained herein are the property of their respective owners and are used for information purposes and only to identify the company names or brands of their respective owners. (060126-#i1)

United Kingdom: This material has been prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners and is distributed in the United Kingdom by Magellan Investment Partners (UK) Limited (FRN: 1037936), an appointed representative of Sentinel Regulatory Services Ltd (FRN: 1007093) which is authorised and regulated by the Financial Conduct Authority. This material does not constitute an offer or inducement to engage in an investment activity under the provisions of the Financial Services and Markets Act 2000 (FSMA). This material does not form part of any offer or invitation to purchase, sell or subscribe for, or any solicitation of any such offer to purchase, sell or subscribe for, any shares, units or other type of investment product or service. This material or any part of it, or the fact of its distribution, is for background purposes only. This material has not been approved by a person authorised under the FSMA and its distribution in the United Kingdom and is only being made to persons in circumstances that will not constitute a financial promotion for the purposes of section 21 of the FSMA as a result of an exemption contained in the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (FPO) as set out below. This material is exempt from the restrictions in the FSMA as it is to be strictly communicated only to 'investment professionals' as defined in Article 19(5) of the FPO.

United States: This material has been prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners (‘Magellan’) which is a registered investment adviser. The investment strategies described herein are offered in the United States by Magellan Investment Partners North America, Inc., a U.S.-registered investment adviser. Magellan and Magellan Investment Partners North America, Inc. are affiliated entities for purposes of the Investment Advisers Act of 1940. Registration as an investment adviser does not imply any level of skill or training. This material is not intended as an offer or solicitation for the purchase or sale of any securities, financial instrument or product or to provide financial services. It is not the intention of Magellan to create legal relations on the basis of information provided herein. Past performance does not guarantee future results. Where performance figures are shown net of fees charged to clients, the performance has been reduced by the amount of the highest fee charged to any client employing that particular strategy during the period under consideration. Actual fees may vary depending on, among other things, the applicable fee schedule and portfolio size. Fees are available upon request and also may be found in Part 2 of Magellan’s Form ADV.

Canada: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners (‘Magellan’). Magellan is not registered in any province in Canada. The head office of Magellan is in Sydney, Australia and all or substantially all of its assets are situated outside of Canada. Due to the foregoing, there may be difficulty enforcing legal rights against Magellan.

South Africa: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners, who in accordance with FAIS Notice 55 of 2023 issued by the Financial Sector Conduct Authority, Magellan Investment Partners is exempted from section 7(1) of the Financial Advisory and Intermediary Services Act, 2002 (Act No. 37 of 2002). This material is not an offer in terms of Chapter 4 of the Companies Act, 2008.

UAE: This material has been produced by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. This material is not for distribution to any other person. This material, and the information contained herein, does not constitute, and is not intended to constitute, a public offer of securities in the United Arab Emirates (‘UAE’) and accordingly should not be construed as such. Any offer of securities or financial services is made only to a limited number of exempt Professional Investors in the UAE who fall under one of the following categories: federal or local governments, government institutions and agencies, or companies wholly owned by any of them. No securities or services have been approved by or licensed or registered with the UAE Central Bank, the Securities and Commodities Authority, the Dubai Financial Services Authority, the Financial Services Regulatory Authority or any other relevant licensing authorities or governmental agencies in the UAE (the ‘Authorities’). The Authorities assume no liability for any investment that the named addressee makes as a Professional Investor. This material is for the use of the named addressee only and should not be given or shown to any other person (other than employees, agents or consultants in connection with the addressee’s consideration thereof).

Japan: This material is prepared by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. The content is for informational purposes only and directed at Qualified Institutional Investors and other professional investors as defined in the Financial Instruments and Exchange Act. No distribution of this material will be made in any jurisdiction where such distribution is not authorised or is unlawful. This material does not constitute, and may not be used for the purpose of, an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorized or in which the person making such offer or solicitation is not qualified to do so.

Other jurisdictions: This material is provided to you by Magellan Asset Management Limited (ABN 31 120 593 946 AFSL 304 301) doing business as Magellan Investment Partners. No distribution of this material will be made in any jurisdiction where such distribution is not authorised or is unlawful. This material does not constitute, and may not be used for the purpose of, an offer or solicitation in any jurisdiction or in any circumstances in which such an offer or solicitation is unlawful or not authorized or in which the person making such offer or solicitation is not qualified to do so.